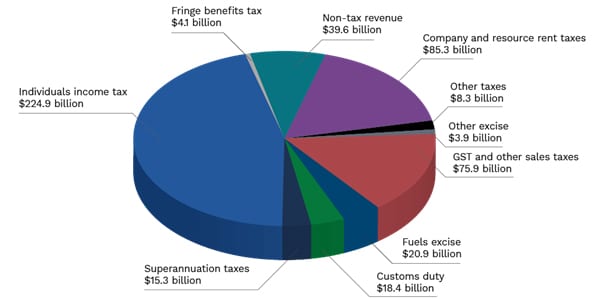

Revenue: Where 2021-22 Budget revenue comes from

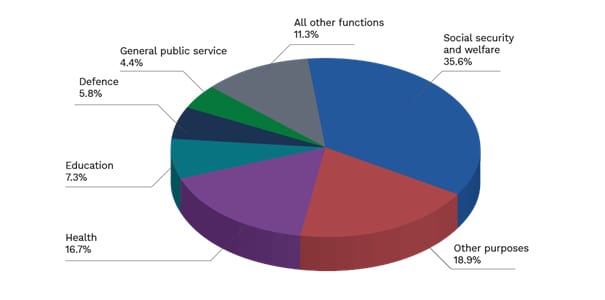

Expenditure: How the 2021-22 Budget is spent

The $2 billion National Mental Health and Suicide Prevention Plan funds a range of initiatives including the enhancement and expansion of digital mental health services, universal aftercare for those who have made a suicide attempt, and a network of Head of Health adult mental health centres and satellites to provide coordinated multi-disciplinary care.

New compliance requirements for NFP income tax exemptions

The Government will invest $1.9m for the ATO to build an online system to enhance the transparency of income tax exemptions claimed by not-for-profit entities (NFPs).

It will be in action from 1 July 2023

Currently non-charitable NFPs can self-assess their eligibility for income tax exemptions, without an obligation to report to the ATO. The ATO will require income tax exempt NFPs with an active Australian Business Number (ABN) to submit online annual self-review forms with the information they ordinarily use to self-assess their eligibility for the exemption. This measure will ensure that only eligible NFPs are accessing income tax exemptions.

| Date of effect | 1 July 2021 | |

|---|---|---|

| Date of effect | Date of Royal Assent of the enabling legislation | |

|---|---|---|

Small businesses with an aggregated turnover of less than $10 million per year will be able to apply to the Small Business Taxation Division of the Administrative Appeals Tribunal (AAT) to pause or modify ATO debt recovery action until their underlying case is decided.

Currently, small business can only pause ATO debt recovery action in the courts. This new avenue will enable a small business to pause ATO debt recovery until their case has been heard by the AAT.

| Date of effect | Grants relating to storm and flood events between 19 February and 31 March 2021 | |

|---|---|---|

Qualifying grants made to primary producers and small businesses affected by the storms and floods will be non-assessable non-exempt income for tax purposes.

Qualifying grants are Category D grants provided under the Disaster Recovery Funding Arrangements 2018, where those grants relate to the storms and floods in Australia that occurred due to rainfall events between 19 February 2021 and 31 March 2021. These include small business recovery grants of up to $50,000 and primary producer recovery grants of up to $75,000.

A range of Government fees and regulatory charges have also been either revised or postponed.

| Date of effect | The first financial year after Royal Assent of the enabling legislation Expected to be 1 July 2022 | |

|---|---|---|

Currently, employees need to earn $450 per month to be eligible to be paid the superannuation guarantee. This threshold will be removed so all employees will be paid super guarantee regardless of their income earned.

The Retirement Income Review estimated that around 300,000 individuals would receive additional superannuation guarantee payments each month once the threshold is removed.

| Date of effect | The first income year after the date of Royal Assent of the enabling legislation. | |

|---|---|---|

The Government will replace the individual tax residency rules with a new, modernised framework. The primary test will be a simple ‘bright line’ test – a person who is physically present in Australia for 183 days or more in any income year will be an Australian tax resident. Individuals who do not meet the primary test will be subject to secondary tests that depend on a combination of physical presence and measurable, objective criteria.

The modernisation of the residency framework is based on the Board of Taxation’s 2019 report Reforming individual tax residency rules – a model for modernisation.

| Date of effect | Losses from the 2019-20, 2020-21, 2021-22 or 2022-23 income years | |

|---|---|---|

Companies with an aggregated turnover of less than $5 billion will be able to carry back losses from the 2019-20, 2020-21, 2021-22 and 2022-23 income years to offset previously taxed profits in the 2018-19, 2019-20, 2020-21 and 2021-22 income years.

The tax refund will be available on election by eligible businesses when they lodge their 2020-21, 2021-22 and 2022-23 tax returns.

Before the measure was introduced in the 2020-21 Budget, companies were required to carry losses forward to offset profits in future years. Companies that do not elect to carry back losses can still carry losses forward as normal.

Let’s look at your “options” to escape the time-for-money trap and thrive, while having more freedom and the lifestyle you want.

This is a loser that most people are probably pretty happy about — the government is extending a task force that targets tax avoidance by multinationals, large public and private groups, trusts and wealthy individuals.

It is giving the Australian Tax Office (ATO) more than $600 million over the next three years to keep the scrutiny on those groups.

The budget forecasts the extension of the task force will make the government $2.1 billion in revenue from tax over the next four years.

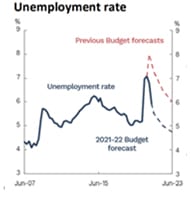

In bad news for people’s pay packets, real wages are not forecast to grow until later this year at the earliest thanks to higher-than-expected inflation.

At the end of last year, Treasury predicted the inflation rate would be 2.75 per cent. The reality has ended up being around 4.25 per cent.

The budget is predicting wages will only be just higher than inflation in the next couple of years, meaning cost of living pressures are unlikely to ease any time soon.

Despite current price hikes, the budget is forecasting inflation will taper off and wages will grow faster by the middle of the decade.

Buried under the wildly exciting headline of Commonwealth’s Deregulation Agenda, is the $19.9 million spend by the Australian Bureau of Statistics to develop a new reporting application to enable businesses to submit surveys on business indicators directly through their accounting software. Excellent. Real time reporting utilising verified data on the state of Australian business. Guarantee of Origin scheme, and the development of a Biodiversity Stewardship Trading Platform to support farmers to undertake biodiversity activities ahead of the introduction of a voluntary biodiversity stewardship market.

Another $148.6m is for the development of community microgrids and just over $50m to develop gas infrastructure projects.

An additional $652.6m has been set aside to extend the ATO’s Tax Avoidance Taskforce by 2 years to 30 June 2025.

In that time, the taskforce is expected to increase receipts by $2.1bn and increase payments by $652.6m.

Just prior to the Federal Budget, the Government announced the extension of the:

|

From |

7:30pm AEDT, 29 March 2022 until 30 June 2024 |

The Government intends to provide a 120% tax deduction for expenditure incurred by small businesses on external training courses provided to employees. The deduction will be available to small business with an aggregated annual turnover of less than $50 million. External training courses will need to be provided to employees in Australia or online, and delivered by entities registered in Australia.

Some exclusions will apply, such as for in-house or on-the-job training and expenditure on external training courses for persons other than employees.

We assume there will need to be a nexus between the employee’s employment and the training program undertaken for the boost, although we are waiting on further details of this initiative to be released.

The boost for eligible expenditure incurred by 30 June 2022 will be claimed in the tax return for the following income year (that is, the 2023 tax return). The boost for eligible expenditure incurred between 1 July 2022 and 30 June 2024, will be included in the income year in which the expenditure is incurred.

|

From |

1 July 2021 |

As previously announced, work‑related COVID‑19 test expenses incurred by individuals will be made tax deductible.

Changes will also be made to ensure that FBT will not be payable by employers if they provide fringe benefits relating to COVID‑19 testing to their employees for work‑related purposes.

The changes for deductions will be effective from 1 July 2021, with the FBT changes to apply from 1 April 2021.

At this stage it is not entirely clear whether the deduction rules will cover expenses incurred where the employee is able to work from home. The initial media release indicates that the measure will cover situations where the individual has the option of working remotely, while the Budget only refers to costs of taking a COVID-19 test to attend a place of work but doesn’t specifically refer to employees who can work from home.

|

From |

1 July 2022 |

This measure has been deferred for 12 months, which means that the tax return lodgement obligation is due to commence from 1 July 2022 with the annual confirmation of ABN details to commence from 1 July 2023.

As announced prior to the Budget, the Government will commit $6.6 million for the development of IT infrastructure that will enable the ATO to share Single Touch Payroll (STP) data with State and Territory Revenue Offices on an ongoing basis.

The funding will be deployed following further consideration of which states and territories are able and willing to make investments in their own systems and administrative processes to pre-fill payroll tax returns with STP data in order to reduce compliance costs for businesses.

The measure that enables payments from certain state and territory COVID-19 business support programs to be treated as non-assessable non-exempt (NANE) income has already been extended until 30 June 2022.

The Government has announced that the following state and territory grant programs have been made eligible for this treatment since the 2021-22 MYEFO, although it is not clear whether the relevant legislative instruments have been issued as yet:

|

From |

1 January 2024 |

As announced prior to the Budget, businesses will be able to report Taxable Payments Reporting System data via their accounting software on the same lodgment cycle as their activity statements.

The measure is expected to reduce the costs of complying with the system and increase transparency.

|

From |

1 January 2024 |

As announced prior to the Budget, companies will be able to choose to have their pay as you go (PAYG) instalments calculated using current financial performance, extracted from business accounting software, with some tax adjustments.

The move is intended to ensure that instalment liabilities are aligned to the businesses cashflow. In addition, the digitisation of PAYG instalments will improve transparency and provide more accurate data on performance.

|

From |

2022-23 income year |

Normally, GST and PAYG instalment amounts are adjusted using a GDP adjustment or uplift. For the 2022-23 income year, the Government is setting this uplift factor at 2% instead of the 10% that would have applied.

The 2% uplift rate will apply to small to medium enterprises eligible to use the relevant instalment methods for instalments for the 2022-23 income year and are due after the amending legislation comes into effect:

| From | 7:30pm AEDT, 29 March 2022 until 30 June 2023 |

The temporary 50% reduction in superannuation minimum drawdown requirements for account-based pensions and similar products has been extended to 30 June 2023.

Minimum superannuation drawdown rates 2019-2023

|

Age |

Default minimum drawdown rates (%) |

Reduced rates by 50% for the 2019-20 to 2022-23 income years (%) |

|

Under 65 |

4 |

2 |

|

65-74 |

5 |

2.5 |

|

75-79 |

6 |

3 |

|

80-84 |

7 |

3.5 |

|

85-89 |

9 |

4.5 |

|

90-94 |

11 |

5.5 |

|

95 or more |

14 |

7 |

|

From |

1 July 2024 |

|

From |

1 July 2021 |

The Medicare levy low income thresholds for seniors and pensioners, families and singles will increase from 1 July 2021.

|

|

2020-21 |

2021-22 |

|---|---|---|

|

Singles |

$23,226 |

$23,365 |

|

Family threshold |

$39,167 |

$39,402 |

|

Single seniors and pensioners |

$36,705 |

$36,925 |

|

Family threshold for seniors and pensioners |

$51,094 |

$51,401 |

For each dependent child or student, the family income thresholds increase by a further $3,619 instead of the previous amount of $3,597.

The Home Guarantee Scheme guarantees part of an eligible buyer’s home loan, enabling people to buy a home with a smaller deposit and without the need for lenders mortgage insurance. The Government has extended two existing guarantees and introduced a new regional scheme.

Just prior to the Budget, the Government announced:

|

From |

April 2022 |

A one-off $250 ‘cost of living payment’ will be provided to Australian resident recipients of the following payments and concession card holders:

From | 1 July 2021 to 30 June 2022 |

The low and middle income tax offset (LMITO) currently provides a reduction in tax of up to $1,080 for individuals with a taxable income of up to $126,000.

The tax offset is triggered when a taxpayer lodges their 2021-22 tax return.

For the 2021-22, the LMITO will be increased by $420 which means that the proposed new rates for individuals are as follows:

Taxable income | Offset |

$37,000 or less | $675 |

Between $37,001 and $48,000 | $675 plus 7.5 cents for every dollar above $37,000, up to a maximum of $1,500 |

Between $48,001 and $90,000 | $1,500 |

Between $90,001 and $126,000 | $1,500 minus 3 cents for every dollar of the amount above $90,000 |

| From | 12.01am 30 March 2022 |

There are a few jokes going around social media about the price of fuel.

As widely predicted, the Government will temporarily reduce the excise and excise-equivalent customs duty rate that applies to petrol and diesel by 50% for 6 months from Budget night. That is, the current 44.2 cents per litre excise rate will reduce to 22.1 cents per litre from Budget night. However, the measure is subject to the passage of the enabling legislation so don’t expect to see a change right away.

The reduction extends to all other fuel and petroleum based products except aviation fuels.

At the conclusion of the 6 months on 28 September 2022, the excise and excise-equivalent customs duty rates revert to previous rates including any indexation that would have applied during the 6 month period.

The Australian Competition and Consumer Commission (ACCC) will monitor the price behaviour of retailers to ensure that the lower excise rate is passed on to consumers.

The measure comes at a cost of $5.6bn.